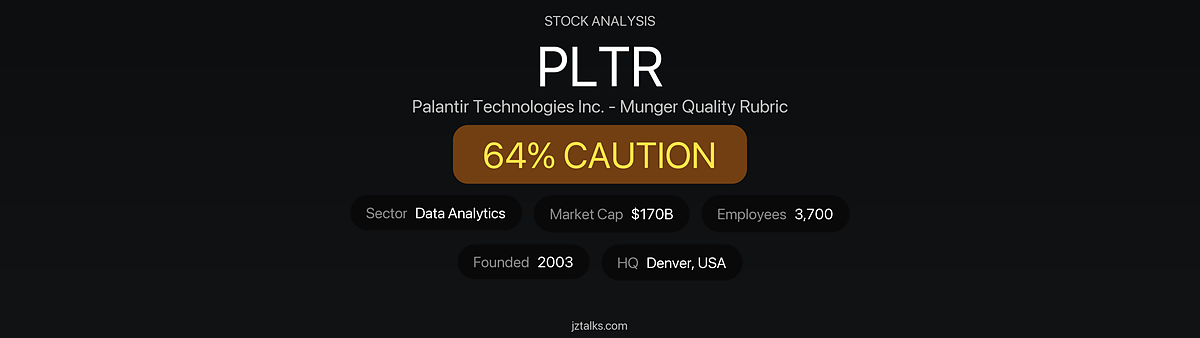

Evaluation Date: 2026-01-14 | ← Back to All Stock Evaluations

Disclaimer: This analysis is for educational purposes only and does not constitute investment advice. Always conduct your own due diligence and consult a qualified financial advisor before making investment decisions. Past performance does not guarantee future results.

Key Takeaways: Is PLTR a Quality Investment?

Munger Quality Score: 135/210 (64.3%) – CAUTION

- Top Strength: Business Quality & Moat (83%) — Proprietary ontology technology with $2.5M-$7.5M switching costs

- Key Concern: Valuation (29%) — P/E of 375x with no margin of safety

- Valuation: 375x P/E vs 107x 5-year average — Significantly overvalued at 28x Graham Number

- Key Risk: Extreme valuation combined with $4B+ insider selling in 2024