View All Stock Evaluations | Evaluation Date: 2026-01-12

Key Takeaways: Is QCOM a Quality Investment?

This section provides a scannable summary for quick reference.

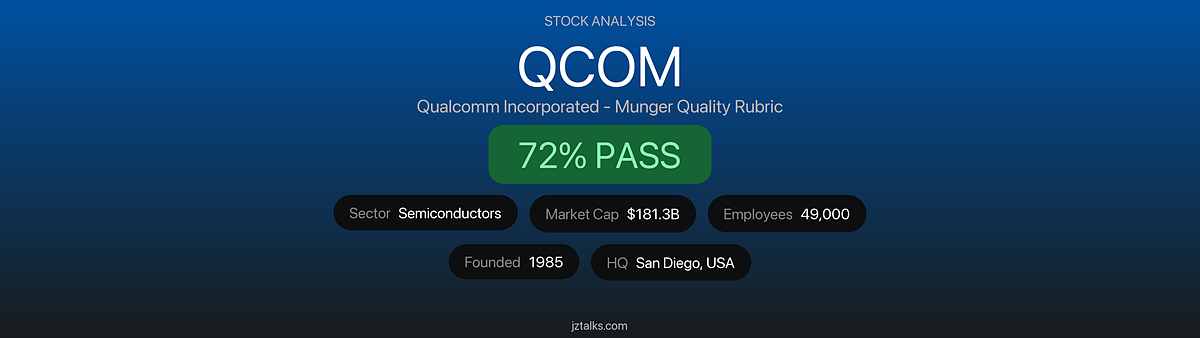

- Verdict: 🟢 PASS — Score: 152/210 (72.4%)

- Moat Strength: Strong — World-leading 5G patent portfolio with high-margin licensing revenue; testing requirements create massive barriers to entry

- Financial Health: Excellent — Debt/EBITDA 0.86x, ROIC 26%, $12.8B FCF, $13.3B cash reserves

- Valuation: Fair to Slightly Overvalued — P/E 34x vs 5yr avg 18x; Forward P/E 14x more reasonable

- Key Risk: 46-64% revenue exposure to China and impending loss of Apple modem business by 2027

This evaluation uses the Charlie Munger Quality Rubric framework analyzing management, moat, financials, and valuation across 8 dimensions.